Amit is a voracious writer and reader with experience in developing content for different niches. A friendly and down-to-earth person with a sense of humor, he is keen on offering factual and informative insights in his writings. He loves researching new developments in the industry and putting them in layman’s terms.

HONG KONG: Investors rushed back into Chinese property developers’ shares and bonds, sparking a strong rebound in the market on Tuesday. After a significant selloff in the previous session, the Hong Kong Hang Seng Mainland Properties Index surged 14%, and the CSI 300 Real Estate benchmark gained 8%, signaling the first monthly gain for the real estate sector after four months of heavy losses.

Country Garden and Country Garden Services, both listed in Hong Kong, rebounded impressively by 18% and 26.5%, respectively, effectively reversing the sharp declines from the day before. Country Garden’s dollar bond due in May 2025 also firmed to 21.675 cents, compared to 15 cents the previous evening. Shanghai and Shenzhen-traded bonds of the company witnessed significant gains as well.

The market rally was ignited by China’s top leaders’ commitment to bolstering policy support for the economy, particularly focusing on boosting domestic demand during the post-COVID recovery. Investors took notice of the change in tone concerning the property sector, speculating that further measures to stabilize the market might be imminent.

The statement by the Politburo, the ruling Communist Party’s top decision-making body, omitted the phrase “houses are for living in, not for speculation,” which led analysts to believe that Beijing might ease property restrictions in the near future.

Shares of major developers like Sunac China, Longfor Group, Seazen Group, and KWG Group all recorded substantial gains, making it the best day for many property stocks since November.

Despite the positive sentiment, analysts remain cautious, expecting any property easing to be limited and potentially targeted on a “city-by-city” basis. The overall market expectations were exceeded by Politburo’s statement, but experts believe that there is no quick fix for the property sector, with the central government likely to make only marginal adjustments to existing restrictive measures in major cities.

Morgan Stanley anticipates a “more sensible and forceful package” from policymakers, which could include easing second-home purchase restrictions in second-tier cities. The recent debt crisis in the property sector had investors worried, but the government’s pledge to support the embattled sector has instilled hope for a recovery.

OfficeBanao, a startup headquartered in Gurugram, has secured funding from three angel investors, which include former Meta India MD Ajit Mohan and former Colliers India CEO Ramesh Nair. The raised funds will be utilized by the startup to enhance its technology-driven platform, accelerate product development, and expand its workforce. OfficeBanao, founded in 2021 by Tushar Mittal, Akshya Kumar, and Divyanshu Sharma, offers AI-powered space planning, 3D walkthroughs, a wide range of product selections, and real-time collaboration.

In April of this year, the startup had already raised $6 million in seed funding led by Lightspeed. OfficeBanao brings together architects, contractors, designers, material suppliers, and office furniture providers to serve various commercial interiors and businesses of all sizes.

In recent developments within the proptech industry, Crib, another startup, raised Rs. 15 crores in its seed round co-led by We Founder Circle and Rebright Partners. Additionally, iDesign.Market, a SaaS startup catering to Interior and Construction Companies, secured $200,000 in pre-seed funding from notable entities like Jaipur Rugs and a consortium of angel investors, including PropTech expert Brigade REAP.

Last quarter, PeProp.Money, India’s largest and leading real estate marketplace raised seed fund from India Accelerator to expand nationwide.

Investing in real estate offers an attractive return on investment, especially over the long term. The pandemic had an impact on every industry, which caused the Indian GDP to shrink by 6.6% in 2020-21. In contrast to predictions, real estate showed remarkable resilience as an asset class by quickly recovering and currently experiencing a surge in demand.

Financial experts recommend investing between 10% and 15% of one’s gross income in order to ensure a prosperous retirement and achieve long-term financial goals. Many people are considering real estate investments as safe and long-term assets in these uncertain times characterized by stock market volatility. Such investments have numerous advantages, allowing investors to reap multiple benefits.

Most investment avenues are now vulnerable to the market’s invisible hand because of market volatility, an uncertain future, and banking failures, among many other factors. But, riding on a wave of housing demand, real estate has established itself as a bounce-back asset class, attracting massive investment from private equity and a variety of other sources.

Real estate investing has grown in popularity over time because it provides greater stability and higher returns than other asset classes. As a result of reforms such as the Real Estate (Regulation and Development) Act (RERA) and the Goods and Services Tax (GST), real estate investment has become more transparent and appealing.

Real estate is a tangible asset that possesses enduring worth. It presents investors with the opportunity to generate rental income or sell the property at a premium. Additionally, it can serve as collateral for securing financing, thereby making it a secure investment comparable to gold. The demand for housing has increased as the world’s population has surpassed 8 billion. The value of real estate is expected to appreciate in a country like India, where there is an unprecedented infrastructure boom and urbanization. Foreign Direct Investment reached a substantial $26.17 billion between April 2020 and December 2021. Notably, India has emerged as one of the top 10 housing markets worldwide in terms of price appreciation, mainly due to rapid urbanization and population growth.

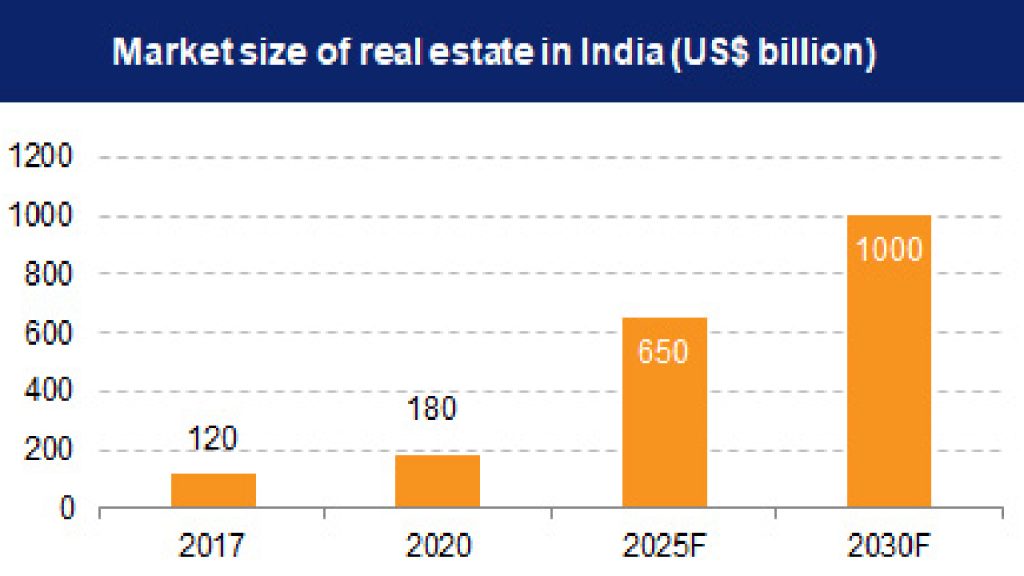

Market Size

The real estate market is predicted to increase from Rs. 12,000 crore (US$1.72 billion) in 2019 to Rs. 65,000 crore (US$9.30 billion) by 2040. In India, the real estate market is anticipated to grow to US$ 1 trillion in size by 2030 from US$ 200 billion in 2021 and to account for 13% of GDP by 2025. Retail, hospitality, and commercial real estate are all experiencing significant growth as well, which is crucial infrastructure for India’s expanding needs.

In the first nine months of FY22, the top eight cities in India’s real estate market saw land deals totaling more than 1,700 acres. From 2017 to 2021, there were 10.3 billion dollars in foreign investments in the commercial real estate market. Following the replacement of the current SEZs Act, developers anticipate a sharp increase in demand for office space in SEZs as of February 2022.

The influx of investors is accelerating the real estate growth trajectory to new heights. Investors are drawn to real estate because it can withstand the uncertainty of the stock market. Real estate offers a sense of security because of its tangible nature, which protects it from market instability. Real estate investing also has the added benefit of tax advantages, solidifying its place as one of the safest avenues for capital preservation and returns.

Market post-pandemic

The nationwide lockdown brought on by the pandemic in 2020 caused the real estate market to slow down. Real estate stood out, demonstrating its resilience and amazing capacity to recover while many economic sectors were hit hard. Real estate experienced exponential growth across tier 1, 2, and 3 cities despite the difficulties encountered, such as elevated construction costs and a significant 225 bps hike in the repo rate. ICRA reports predicted that Indian real estate firms would raise Rs. 3.5 trillion in 2022 through infrastructure and real estate investment trusts.

Post-pandemic, people eagerly rushed to purchase properties. The middle class and upper middle class made significant investments in real estate, boosting its value and supporting the sector, after having saved money during the pandemic. The sizeable private equity investment that India’s real estate has attracted is another factor that contributes to its stability and allure. A Colliers India report claims that during the first half of 2021, when the government was gradually removing the lockdown measures, the Indian real estate market saw a significant inflow of private equity investments totaling US$ 2.9 billion.

The real estate industry has long been known for its fierce competition and ever-changing landscape. Agents and developers constantly strive to find innovative ways to market their properties and captivate potential buyers. In recent times, the advent of mobile augmented reality (AR) has emerged as a game-changing tool, revolutionizing the real estate experience. By seamlessly blending digital information with the physical world, mobile AR is reshaping the processes of property search, presentation, and sales.

One of the most profound impacts of mobile AR in the real estate sector lies in its ability to enhance the property viewing experience. Gone are the days when prospective buyers had to physically visit each property to grasp its layout, features, and ambiance. With mobile AR, users can now embark on virtual property explorations from the comfort of their own homes. By simply directing their smartphones or tablets toward a property listing, users unlock a treasure trove of information, including detailed floor plans, interactive 3D models, and even immersive virtual walkthroughs. This not only saves time and effort for both buyers and agents but also creates a more engaging and immersive experience.

Furthermore, mobile AR has become an invaluable tool for property developers and architects. By harnessing the potential of AR technology, they can construct interactive 3D models of their projects, allowing potential investors and buyers to visualize the end product long before construction commences. This proves particularly beneficial for off-plan properties, where decisions are often made based on nothing more than blueprints or artistic impressions. Mobile AR empowers developers to present an accurate and tangible representation of their vision, instilling confidence in potential buyers and driving sales.

Beyond enhancing property viewing experiences, mobile AR is reshaping the landscape of property marketing. By integrating AR elements into their marketing materials, agents can create captivating and interactive content that truly captures the attention of potential buyers. Static images are now being replaced by dynamic, 360-degree virtual tours, enabling users to explore properties in a more immersive and realistic manner. Furthermore, mobile AR allows for the creation of interactive property brochures and location-based advertisements, accessible to users as they explore specific neighborhoods or areas.

The advancements in mobile AR technology also hold immense potential for data analysis and decision-making within the real estate industry. By collecting and analyzing data from AR interactions, agents can gain invaluable insights into user behavior and preferences, which can inform effective marketing strategies and even influence the design and development of future properties. For instance, if a particular feature or layout proves exceptionally popular among users, developers may opt to incorporate it into upcoming projects, resulting in the creation of more desirable and marketable properties.

In conclusion, mobile augmented reality is disrupting the real estate industry, offering an array of benefits for agents, developers, and buyers alike. With its capacity to enhance property viewing experiences, revolutionize marketing strategies, and provide invaluable data insights, mobile AR is reshaping the way properties are perceived, marketed, and ultimately sold. As technology continues to evolve and become increasingly accessible, mobile AR is set to become an integral part of the real estate landscape, shaping the industry’s future for years to come.

The Rent Control Act in India is the primary legal instrument that governs rent regulation, landlord rights protection, and tenant rights.

Summary of the Rent Control Act

The legislature enacted a national Rent Control Act in 1948. It controls the guidelines for renting out a property and makes sure neither the rights of the landlords nor the tenants are violated by each other. It should be noted that each state currently has its own Rent Control Act, and while they are generally similar to one another, they do have a few small variations.

The 1948 Act was quite restrictive and pro-tenant, which has made some sectors of the real estate market struggle to expand. Despite inflation and rising property values, some properties that have been rented out since 1948 continue to pay the same amount of rent.

In an effort to prevent the property’s value from declining, the Central Government attempted to change the Act in 1992 through a proposed model. The sitting tenants, unfortunately, resisted the adjustments, so they did not go into effect.

Rental Agreement

In India, renting or letting out any property for residential or commercial purposes is subject to a number of laws and restrictions, including: – According to the legislation, it is necessary for the two parties to have a written agreement outlining all the terms and circumstances of the tenancy.

In the following circumstances, an agreement formed without being explicitly set forth in writing is not a binding contract:

All modifications, irrespective of the nature of the correction, must also be made in writing.

Both the landlord and the renter must sign the document and both parties’ signatures must be dated.

The contract needs to be registered and stamped.

The obligations of both the landlord and the tenant cannot be enforced or legally protected in the absence of a formal rental agreement.

As a result, it is generally advisable to get the assistance of a legal professional when creating such an agreement due to the numerous complications involved, especially in commercial leasing.

Tenant’s Rights

The Rent Control Act was created to safeguard both tenants’ rights as well as those of landlords and their property. The Act grants the tenant a few key rights, including the following:

Right Against Unfair Eviction: In accordance with the Act, the landlord is not permitted to remove the tenant without a valid reason or justification. Each state has a slightly different set of eviction laws. In some places, the landlord must go before the court and request a court order before they can evict a tenant. If the renter is ready to accept any adjustments to the rent, he or she cannot be evicted in several states.

Fair Rent: The landlord is not allowed to demand excessive rent while renting out a home. A rental property’s appraisal must take its value into consideration. The tenant may go to court to seek relief if they believe the amount of rent being requested is excessive given the worth of the property. Typically, the rent should range from 8% to 10% of the total value of the property, which includes all costs associated with building and property improvements.

Essential Services: The renter has a fundamental right to use vital services like power and water supply. Even if the renter has not made rent payments for the same or a different property, the landlord does not have the right to terminate these services.

Landlord’s Legal Rights

The property is always the focal point of a rental agreement, and it must be safeguarded from unfair exploitation. The following rights belong to the landlord under the Rent Control Act:

Right to Evict: Each state has a varied set of laws governing the ability to evict a tenant. Meaning that in some places, a landlord has the right to remove a tenant for legitimate, personal reasons such as wishing to move in. In Karnataka, such a justification is not a valid ground for eviction. In most situations, the landlord must file a court petition to evict the tenant. Additionally, before going to court, the landlord is required by law to give the tenant adequate notice.

Charge Rent: As the property’s owner, the landlord is entitled to charge rent to a tenant. As there is no legal law establishing a cap on rent, the landlord is free to keep raising the rent fees as he sees fit. Hence, it is wise to include the amount of the increase and the conditions of the increase in the rental agreement itself in such circumstances. The rent often goes up by 5% to 8% on a yearly basis.

Temporary Repossession of Property: The landlord has the right to temporarily take back possession of the property in order to repair, change, or improve it. Nonetheless, such alterations to the property must not do the tenant any harm or seriously interfere with his tenure.

Absence of the Rent Control Act’s application

When a property has been rented out, there are some circumstances in which the Rent Control Act is not applicable. As follows:

Property leased to private limited or public limited firms with a paid-up share capital of Rs. 1 crore or more.

Property leased or subleased to banks, corporations created under state or federal law, or public sector operations.

Property rented to foreign businesses, missions abroad, or international organizations.

6 Steps to Rent Commercial Property in India

Since there is fierce internal rivalry in the Indian real estate market, rental agreements must be carefully negotiated. You must be aware of all applicable laws for your type of business and the appropriate questions to ask.

Verifying title ownership

Always make sure you have full knowledge of who owns the property, therefore, having access to the title deed is necessary to verify the rent. Before entering into a contract with the landlord, conduct more research to make sure there is no sub-rent or other type of rent associated with the property.

Plans approved and Powers of attorney (PoA)

It is generally essential to check the title deed and commencement certificate given by the relevant authorities if the property you are renting is under construction. Make sure to verify the occupation certificate before renting out commercial space on a built-up property. In the case of indirect rent, it’s also crucial to verify whether any kind of power of attorney exists.

A suitable rental agreement

Make sure the rental agreement is adequate based on operations before engaging in any type of mutual commitment with the landlord. Whether it is a rental leasing agreement or an agreement for co-working office space, be precise about the type of rent.

Verification of Income Tax and Mortgage

In the case of a business agreement, it is usually advisable to investigate the landlord’s tax history to see whether there are any current legal problems or investigations. You can use this to find out if the property in question falls under the Development Control Rules’ “business” or “residential” classification under the Income Tax Act of 1961. You can later be assessed a TDS if there is any ambiguity in this classification.

Checking the property agent’s history

When hiring a real estate agent, it’s crucial to research his credibility. Past rental agreements and word of mouth are other good ways to learn more about the agents. Demand that the agents provide information on previous clients they have served. Their reluctance to do so may be a blatant sign of past dishonest behavior, if any.

Validity of the Rent Agreement

A business leasing agreement must have the following key details in addition to other clauses:

Date of commencement and termination

Property location

The total cost of the rental as well as the details of the deposit.

Payment Intervals

Renewing lease conditions

The names of each party and their signatures.

Required documents for a commercial lease agreement?

Aadhar card, receipt, or any other kind of official identification

The original passport must be submitted; if it is not, an Indian Power of Attorney must be shown if the ID is proving another person for the registration.

Proof and the Kind of Business Established

Authentic copy of ownership documentation for the rental property

Approvals from the government, if any Two recently taken passport-size photos.

Print the Business Rental Agreement on the recommended-value stamp paper.

Articles of Association, Memorandum of Association, If any

shareholder and listing agreements, if any

bonds and dealership proofs, if any

associations of person’s understanding, if any

What steps must be taken to utilize the commercial rental agreement?

Each party, including the guarantor, shall receive a copy of the completed document. Given the length of the paper, each side should be given the chance to read it, which could take some time.

The Business Rental Agreement must be printed on “non-judicial stamp paper” or “e-stamp paper,” both of which are readily available in any state. The “duration” of the rent and the state in which it is implemented would determine the value of the stamp paper.

After printing the rental agreement on stamp paper or e-stamp paper, as appropriate, both parties must sign it. Moreover, a copy of the Commercial Rental Agreement should be kept by each party.

The Commercial Rental Agreement must be registered if the rental length is more than 11 months. For the purposes of registration, both the lessor and the lessee must visit the sub-registrar’s office.

Disclaimer: Access to the content on this internet page is provided by iPropUnited as a courtesy to the public for educational reasons based on related news and stories. The accuracy of any information on this website cannot be guaranteed, however, it is all believed to be credible.

Yashovardhan Birla, a scion of the renowned Birla family, has emerged as a remarkable individual with his own unique achievements. Beyond his family’s wealth and influence, he has established himself as a capable leader and entrepreneur in the corporate world. Let’s delve into Yashovardhan Birla’s journey, educational background, net worth, and dedication to fitness.

Yashovardhan Birla, also known as Yash Birla, is the head of the Yash Birla Group, a prominent business conglomerate based in India. Born on September 29th, 1967, in Mumbai, India, Yash faced profound tragedy in 1990 when he lost both his parents and his sister in a devastating accident. Despite the immense personal loss, he took over the reins of the family business at the age of 23 while pursuing his business administration studies in the United States, displaying remarkable leadership skills and determination.

Yash Birla received his secondary schooling in Mumbai before enrolling at an HR college in the same city. Later, he pursued a degree in Business Administration from a university in the USA. However, Yashovardhan Birla has also faced legal challenges in recent years, as he was declared a willful defaulter by the UCO Bank for unpaid loans from his now-defunct company, Birla Surya Ltd. He has been engaged in legal battles to resolve this issue.

In addition to his entrepreneurial endeavors, Yashovardhan Birla is renowned for his dedication to fitness. Despite being 51 years old, he remains a fitness icon, maintaining an impressive physique and leading a healthy lifestyle. Notably, he abstains from alcohol, prioritizing his physical well-being.

Yashovardhan Birla’s Luxurious Lifestyle and Net Worth

Hailing from a wealthy family, Yashovardhan Birla enjoys a lavish lifestyle, boasting luxurious properties both in India and abroad. One of his notable possessions includes a mansion in South Mumbai. He is also an avid car enthusiast and can often be seen driving high-end luxury vehicles. As of late 2022, Yash Birla’s net worth stands at an impressive $5 million, according to Birla Healthcare.

Yashovardhan Birla’s life exemplifies resilience, determination, and entrepreneurial spirit. Beyond the legacy of his family, he has carved a distinct path for himself, becoming an inspiration to many through his accomplishments in business and commitment to fitness.

Simpliforge Creations, a leading provider of additive manufacturing solutions, has introduced a groundbreaking innovation—their state-of-the-art Robotic Construction 3D Printer. This printer, claimed to be the largest in South Asia and the first of its kind in India, was inaugurated by Sri Thaneeru Harish Rao, Hon’ble Minister for Finance, Health and Family Welfare, Govt. of Telangana.

Unprecedented in size and capabilities, Simpliforge’s Robotic Arm Construction 3D Printer is capable of creating full-scale civil structures, as well as printing landscaping elements, furniture, statues, and wall façades. It utilizes eco-friendly materials like geopolymers and clay, and Simpliforge has also introduced their proprietary construction material, ‘SIMPLICRETE,’ for use with the printer. By harnessing the advantages of Additive Manufacturing, such as minimal wastage, streamlined supply chains, optimal resource utilization, and decentralized manufacturing, the construction industry is set to experience a transformative shift.

During the launch event, Hon’ble Minister Harish Rao expressed his enthusiasm, stating, “Innovation can thrive anywhere, not just in Tier I Metro cities, but even in small towns like Siddipet. This 3D printer is a remarkable milestone. I am delighted to inaugurate this state-of-the-art technology at Charvitha Meadows. I congratulate the entire team of Simpliforge for this remarkable achievement and extend my best wishes to continue contributing to their industry, positioning Siddipet as a hub for advanced technology innovations.”

Amit Ghule, Founder & COO of Simpliforge Creations, expressed his delight, stating, “We are honored to have Hon’ble Minister Harish Rao Garu join us in launching our project. Our current 3D printer can construct structures up to 7m in size, making it the largest Robotic Concrete 3D Printer in India and the entire South Asian region. Moreover, the printer’s range can be expanded as per requirements. The Robotic Concrete 3D printer offers enhanced design versatility and flexibility for designers, while also being easy to deploy at project sites compared to gantry-style printers, making it appealing to architects and developers.”

Dhruv Gandhi, Founder & CEO of Simpliforge Creations, added further details about the technology, saying, “At Charvitha Meadows, we are printing various artistic elements for its Sanjeevani Park, positioning it as India’s first park of its kind. The design philosophy of Charvitha Meadows revolves around sustainable living and the integration of futuristic technologies. The selection of this Robotic 3D printing technology is based on its ecological advantages and the design freedom it offers. We deeply appreciate the Telangana Government for consistently promoting innovative technologies and their efforts towards establishing a ‘National Centre for Additive Manufacturing,’ showcasing their proactive interest in advancing this technology.”

With an extensive materials library, specialized design expertise, and profound domain knowledge in technology applications, Simpliforge Creations aims to expand globally with its revolutionary technology. The company envisions constructing unique civil structures while advancing robotic technology to enable smart construction both in India and abroad. This technology empowers architects and structural engineers with unparalleled design freedom, allowing them to experiment with novel and distinctive structures for innovative construction projects.

Buying real estate can be a smooth process, but selling a property often poses significant challenges. When considering a property purchase, buyers tend to focus on location, specifications, and budget. However, when it comes to selling after a few years, the quoted price by brokers often falls short of expectations.

Before making a property purchase, it is crucial for homebuyers to assess the ease of selling it if the need arises. Whether it’s upsizing to a bigger house, funding education abroad, or dealing with financial crises, the property’s location plays a vital role. Proximity to the central business district, access to main roads, and the presence of schools, hospitals, markets, theaters, restaurants, and malls in the vicinity significantly impact the ease-of-exit quotient.

The success of selling a property also depends on factors such as the project’s location, available amenities, and the type of residents. Exclusive projects with film stars, CEOs, and NRIs as investors or residents tend to appreciate faster than affordable offerings in peripheral locations where even maintaining a swimming pool can be a challenge.

Moreover, the track record of the developer and the quality of amenities in a gated community influence the ease or difficulty of selling an apartment. Developers with a proven history of timely project delivery instill confidence in potential buyers, while well-maintained amenities contribute to a property’s appeal.

Different perspectives come into play when considering selling property. End-users typically hold onto their apartments until they upgrade or face emergencies, while investors focus on capital appreciation. The issuance of an occupancy certificate usually leads to an increase in property prices, and new supply in the area can also affect the market dynamics.

Experts advise caution when dealing with first-time builders, suggesting that investors consider investing in projects by reputable developers during the early stages and exiting after two years of possession for optimal profitability. Demographics and the maintenance standards of a housing society also influence the ease of exit. Factors such as premium maintenance, the quality of residents, and proximity to the central business district play significant roles in determining a property’s value.

It’s important for property sellers to maintain reasonable expectations when it comes to pricing. Comparing a six-year-old property to a brand-new project with contemporary design and amenities will likely result in unrealistic pricing expectations. Additionally, ensuring clear title ownership and proper legal documentation is essential for a smooth property sale.

By understanding these factors and setting realistic expectations, property sellers can navigate the challenges and increase their chances of a successful and profitable sale in the competitive real estate market.

In India, there are numerous real estate laws that differ between States. The Real Estate (Regulation and Development) Act of 2016 (RERA), the Transfer of Property Act of 1882, and the Registration Act of 1908 are some crucial laws that have an impact on the nation’s real estate market. Therefore, it is essential to have a fundamental awareness of these regulations if you intend to invest in real estate or already own property.

Indian real estate is governed by a mix of central laws and state-specific regulations. The Indian Constitution’s concept of “land” is the basis for this system. According to Article 246, “land” is one of the topics covered by List 2 or the State List of the Seventh Schedule, which only States are permitted to regulate. Contrarily, List 3 or the Concurrent List of the Seventh Schedule to the Indian Constitution includes topics that are subject to both federal and state legislation, including “Transfer of property other than agricultural land, registration of documents and deeds,” “Contracts other than for agricultural land,” and “Transfer of property other than agricultural land.” Real estate in India is linked to land-related issues because properties are strongly related to varied laws.

The fact that India is a nation with numerous sects and that its rules on inheritance and devolution, among other things, draw heavily upon diverse practices and customs in addition to codified laws, is another factor that contributes to the formulation of the laws. Many rulings and legal precedents on various real estate dynamics have also been established over the years. Depending on the court or venue that rendered the decision, these judgments have either increased the sector’s dependability or increased its legal stipulations.

Indian Real Estate Laws

the Registration Act of 1908 and the Indian Stamp Act of 1899

These acts regulate the rules pertaining to the requirement for the registration of various deeds, instruments, and papers pertaining to the transfer of an interest in immovable property and the payment of stamp duty on said documents.

Regulatory and Development of Real Estate Act of 2016 (RERA)

To protect investors’ interests, the Real Estate Act of 2016 monitors the construction, promotion, and sale of real estate developments. The Real Estate Regulatory Authority and the Appellate Tribunal were established as alternative dispute resolution mechanisms under the Act. Additionally, it requires any real estate developments that fall under its purview to be registered. To ensure that federal legislation is carried out locally, many states have enacted similar RERA rules.

Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Act, 2013

In the event that private land parcels are acquired by the government for a business or certain public uses, this Act assures that families and people are fairly paid. It broadly outlines the compensation and remedial actions that the government will take in the case of property or land acquisition.

Transfer of Property Act, 1882

The Transfer of Property Act, 1882 is a crucial law that establishes the fundamental rules of ownership for immovable property, including exchange, sale, lease, mortgage, and gift of property.

Indian Easement Act, 1882

The Indian Easement Act of 1882 permits the owner of a property to use it for a predetermined amount of time. It merely explores the numerous aspects of using a property but not having possession of it.

Indian Contract Act, 1872

The laws governing contracts in India are governed by this act, including but not limited to the legal competence to enter into a contract, its execution, enforcement, and breach, as well as the remedies accessible to the signees in the event of any inconsistencies. Contract-related parts and chapters of the Transfer of Property Act, 1882, are considered to be a component of this legislation.

Codes for Land Revenue

The laws governing land revenue, tenancy types, agricultural land holding, and other related issues have been developed by many States around the nation. The mentioned code includes the division and classes of immovable property in a State, transfer limitations, responsibilities and authority of tax officers, and guidelines and sanctions for code violations.

In addition to the laws listed above, several state, local, or municipal laws, customs, and regulations also apply to the real estate industry in India. These subtleties relate to, among other things, Special Economic Zones (SEZs), rent control, urban development, property tax, ownership of property, land pooling, land ceiling, land zoning, and land usage.

An immovable asset’s depreciation is frequently taken into account when determining its price in order to determine how much value has diminished over time. Property depreciation is a frequent occurrence, and if measured correctly, you may quickly ascertain its resale worth.

What is property depreciation?

A decrease in the selling price of an immovable item is all that depreciation in value entails. The land is the only object that has a long lifespan and can continue to be beneficial. Even if the structure’s value decreases with time, the value of the land changes in the other direction. So, only the structure built on the ground is taken into account when calculating the depreciation of property. Buildings and homes lose value with time based on how long they will still be usable. The land, on the other hand, is still valued today.

How is property depreciation determined?

An independent home has an average usable life of about 60 years. The entire useful age of the structure and the number of years following construction must be taken into account when calculating the depreciation of property.

The number of years following construction is divided by the structure’s overall useful age in the calculation used to determine depreciation of property. The current price of the building can be calculated by deducting the formula’s result from the selling price of the building or residence. That, however, does not represent the full cost of the property.

The cost of the land should also be taken into account.

Let’s use an illustration to better grasp this.

For instance, a person wants to sell his ten-year-old house, which-

Land cost Rs. 30 lakh at the time of purchase.

Cost of construction is Rs. 20 lakh.

Land value has increased to Rs 45 lakh.

The maximum useful age is 60.

Age of the structure in years since construction is 10 years.

As a result, using the formula above,

The property’s depreciated value is 10/60, or 1/6.

To get the property’s market worth, subtract this depreciation from the building cost and add the increased land value.

Building cost after depreciation = Rs. 20,00,000* (1/6) = Rs. 3.33 lakh

= Rs 20 lakh – Rs 3.33 lakh

Rs 16.66 lakh

Add the increased land value of Rs. 45 lakh to this.

Hence, the final market value that a person might state is around Rs 61.67 lakh.

Why does the Income Tax Agency publish depreciation rates for buildings?

The Income Tax Department permits taxpayers to claim a deduction based on the decline in the value of their tangible (like real estate) and intangible (like patent) assets. Hence, the tax agency releases the depreciation rate at the beginning of each Financial Year (FY).

Since the Assessment Year (AY) 2018–19, the building depreciation rates have not altered. Buildings fall under a variety of property types. While some structures might be residential, others might be industrial or commercial.

The rate of depreciation for a property is 5% for residential properties and 10% for other buildings. A building’s furniture and fixtures, including its electrical fittings, depreciate at a rate of 10% as well. Temporary wooden constructions depreciate at a rate of 40%.

Factors that cause a property’s value to decline

Physical Obsolescence

Buildings decay with time. A home that has only recently been built needs less care than one that is ten years old because weather conditions can affect the structure’s durability and appearance. So, if a property is older, the depreciation will be greater unless the owner takes good care of it.

The physical upkeep of a property has a significant impact on its depreciation value, according to Sanjeev Bansal, proprietor of Bhagwati Infra. When compared to a well-kept property, a poorly maintained property can experience a 40% greater depreciation. Moreover, properties in underdeveloped locations may depreciate by as much as 60% more than a comparable property in a wealthy neighborhood.

Location and amenities

Homes lose value more quickly in some places than others. A property located in a luxury neighborhood will depreciate less quickly than one in a less affluent neighborhood. In addition, the resale value of the property may potentially be impacted by incomplete or delayed infrastructure projects. For instance, any connectivity project that is currently under construction in your region but has been long-stalled or shelved may result in a considerable decline in property value. Moreover, the construction of slum tenements or a crematory close to the property could have a negative effect on its value.

legal disputes

In general, purchasers avoid buying contested real estate or assets that are mired in legal disputes, although many buyers who are savvy enough to avoid legal disputes might prefer disputed real estate.

The main cause of this is that contested properties are offered for sale for a low price since the sellers just care about making a profit. Their only goal is to sell the property.

Considerations for property depreciation

Although it cannot be avoided, the price of a property is not completely determined by the depreciation formula when it is being sold. If a home has been on the market for a while but has not had any inquiries, the seller may think about lowering the price they have quoted. After figuring out the depreciation value, this decrease will be extra to the price stated.

Also, if a property needs work, the seller might think about doing a little of it before listing it for sale to make sure there are at least a few buyers. Simply put, even if pricing is influenced by the depreciation parameter, it cannot be the sole component used to determine the sale price.

The seller is advised to maintain a negotiation threshold of roughly 10% to close the deal.

Exceptions to property depreciation

An emotional attachment

An individual may occasionally develop a strong emotional bond with a property they own. In that situation, even if the seller excludes the depreciation factor, they can still pay more for the property. For instance, even though the quoted value is more than those of other comparable homes in the region, a person who spent his childhood in an ancestral property that was sold for any reason may decide to repurchase it. He has an emotional attachment to the asset, which is why.

Lack of land

In large cities or prominent places, property owners might command a higher price. This is due to the limited availability of developable land in such areas. As a result, residential prices increase more quickly than those of developing communities with plenty of available land.

In general, property depreciation should be understood by sellers in order to set a fair asking price. Finding the right buyers can be challenging for overpriced properties. Finding the optimum price and a qualified buyer for the property might be aided by calculating the depreciation using the technique previously outlined.

OfficeBanao, a startup headquartered in Gurugram, has secured funding from three angel investors, which include former Meta India MD Ajit Mohan and former Colliers India CEO Ramesh Nair. The raised funds will be utilized by the startup to enhance its technology-driven platform, accelerate product development, and expand its workforce. OfficeBanao, founded in 2021 by Tushar Mittal, Akshya Kumar, and Divyanshu Sharma, offers AI-powered space planning, 3D walkthroughs, a wide range of product selections, and real-time collaboration.

OfficeBanao, a startup headquartered in Gurugram, has secured funding from three angel investors, which include former Meta India MD Ajit Mohan and former Colliers India CEO Ramesh Nair. The raised funds will be utilized by the startup to enhance its technology-driven platform, accelerate product development, and expand its workforce. OfficeBanao, founded in 2021 by Tushar Mittal, Akshya Kumar, and Divyanshu Sharma, offers AI-powered space planning, 3D walkthroughs, a wide range of product selections, and real-time collaboration.

")

in Modern Business")